“Ooh, a storm is threatening.

My very life today.

If I don’t get some shelter.

Ooh yeah, I’m gonna fade away.

War, children, it’s just a shot away.

It’s just a shot away.”

-The Rolling Stones; “Gimme Shelter”

I was driving home from work the other day when “Gimme Shelter” started playing. I’ve always enjoyed the song, but this time, the opening lyrics prompted me to think about the state of global affairs, making it a fitting introduction to our discussion. We have plenty of negative news or noise out there, including an ongoing war in the Ukraine, an escalating war in the Middle East, and a U.S. Presidential election where the candidates make it sound like we are headed into oblivion if one party is elected over another. So, in this Insight we will discuss how we manage through the “noise” and position the Lee Financial portfolio.

MANAGING THROUGH THE NOISE

After my drive home from work, I looked up the genesis of the song “Gimme Shelter.” It was primarily about the horrors of the Vietnam War but also all the tension and turmoil that was gripping the U.S. in the 1960s. While I wasn’t alive in the 1960s, history classes taught me that this was perhaps one of the most tumultuous decades in modern U.S. history. Here’s a quick summary of major events gripping the 1960s.

Civil Rights Movement

- The fight against racial segregation and discrimination reached its peak, with landmark legislation such as the Civil Rights Act of 1964 and the Voting Rights Act of 1965 passed to end racial segregation and protect voting rights.

- Widespread protest, civil disobedience and violent resistance from segregationists (Selma to Montgomery marches, Watts Riots) exposed deep societal divisions.

Vietnam War and Anti-War Protest

- The Gulf of Tonkin incident in 1964 led the U.S. to engage more directly in the Vietnam War, leading to tens of thousands of American casualties and significant controversy.

- The War sparked a large and vocal anti-war movement, particularly on college campuses, with protests sometimes turning violent.

- The 1968 Tet Offensive intensified public opposition and distrust toward the U.S. government’s handling of the War.

Assassinations

- 1963 – President John F. Kennedy was assassinated in Dallas, leading to widespread grief and uncertainty.

- 1965 – Malcom X was assassinated, further fueling racial tension.

- 1968 – Both Martin Luther King, Jr. and Senator Robert F. Kennedy were assassinated, sending shockwaves across the U.S. and leaving a leadership vacuum.

Social and Cultural Upheaval

- The Counterculture Movement saw young Americans reject traditional norms, advocating for civil rights, sexual liberation, environmentalism, and an end to the Vietnam War.

- The Women’s Liberation Movement gained momentum, challenging gender roles, workplace inequality, and reproductive rights.

- The era also saw a rise in the gay rights movement, with events like the Stonewall Riots in 1969 marking the beginning of a new chapter in LGBTQ+ activism.

Political Events

- The 1968 Democratic National Convention was a flashpoint of violence and chaos, with anti-war protests and police clashes broadcast live on TV, highlighting the division within the country.

- The election of Richard Nixon in 1968 represented a shift in the political landscape, with his appeal to the “silent majority” and the beginning of a more conservative backlash against the social changes of the decade.

Cold War Tensions

- The Cuban Missile Crisis in 1962 brought the U.S. and the Soviet Union to the brink of nuclear war, leading to widespread fear and anxiety.

- The Space Race was in full swing with the U.S. landing on the moon in 1969.

Looking over that list is sobering, but at the same time, I bet you can easily overlay current political and cultural tensions as well as other global macro tensions onto that list. Currently, most of the noise we hear is coming from the U.S. Presidential election and wars.

POLITICS AND INVESTING

Elections always seem to add an extra element of uncertainty, and because markets don’t like uncertainty, volatility typically increases. Compounding this volatility is a deluge of media attention and plenty of attack ads with “over the top” comments from candidates along with overexaggerated claims. All this inevitably raises the blood pressure or causes frustration in people who don’t subscribe to the opposing candidates’ views. As we have stated before, volatility is not risk. We also need to remember that volatility—and political viewpoints for that matter—tend to increase psychological reactions in people. These behavioral biases are not always good for us, especially when related to investing.

The Lee Financial solution is to not let how you feel about politics dictate how you think about investing. It is best for you to express your views at the ballot box rather than through changes in your portfolio to time an outcome or political viewpoint. The rationale for this conclusion includes:

- Behavioral biases cloud people’s perception of economic activity.

- The economy and the markets tend to do well under all configurations of government.

- While governmental policies are important, enactment of them isn’t guaranteed, and/or the intended effect may be different than expected.

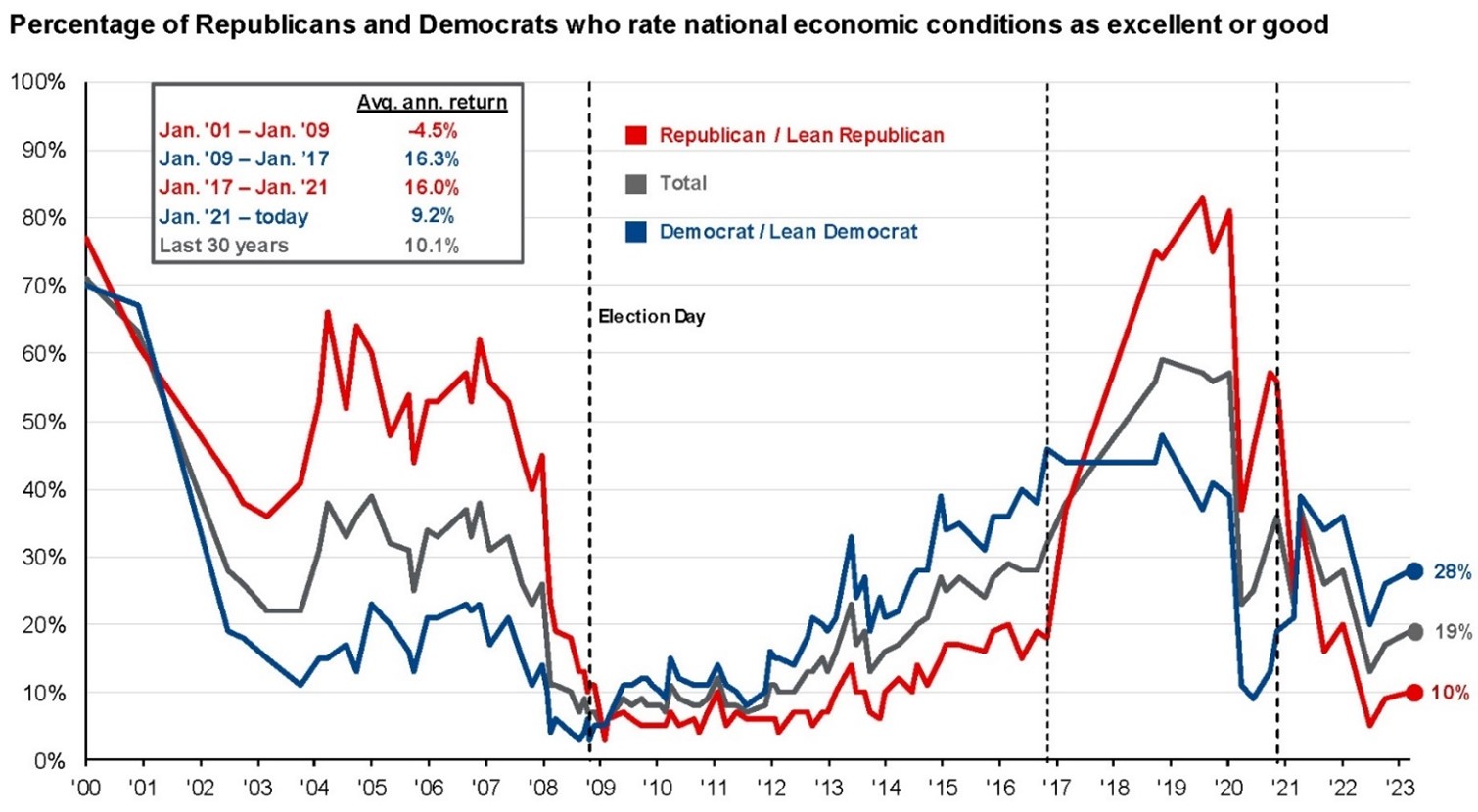

Let’s first address behavioral biases. Below is a survey from the Pew Research Center that asks Americans how they feel about economic conditions. As might be expected, Republicans often feel better about the economy under a Republican president, while the same is evident for Democrats when there is a Democratic President.

But as seen above, the average annual return of the stock market during the Trump administration was 16.0%, almost identical to the 16.3% average annual return during the Obama administration. Looking at a longer time frame (see below), we also see the U.S. economy and stock market have historically done well regardless of who was running the country.

At Lee Financial, we typically make portfolio decisions based on various elements that include economic forecasts, long-term trends, and portfolio diversification benefits to name a few. Importantly, we do our best to make objective decisions as free as possible from behavioral biases. Because political beliefs are highly psychological and hence induce behavioral biases, placing them into the equation can result in mistakes that negatively impact your portfolio.

To further drive this concept home, look at the chart to the right. The chart covers a hypothetical $10,000 investment in the S&P 500 in 1953. And it compares three scenarios: (1) only invested when a Republican is in the White House, (2) only invested when a Democrat is in the White House, and (3) a buy and hold no matter who is in the White House. The results speak for themselves.2

Next up are policy agendas. Policy agendas can be very consequential, and we closely monitor what is advertised and the potential outcomes that may result. However, we understand that the promotion of a specific policy agenda by a candidate or party neither guarantees the administration will be able to enact those policies, nor that the intended impacts will be realized.

A perfect example of this phenomenon comes in the energy sector. Most would assume that fossil fuels should do well under Republicans, and green energy should do well under Democrats. As seen below, the opposite recently happened.

President Trump campaigned heavily to support the traditional energy industry and followed through while in office by approving leases for drilling activity. President Biden campaigned on scaling back fossil fuels and championing renewable energy and followed through after elected.3

Despite Trump’s policy agenda, during his administration the S&P 500 Energy index was down -40%, while the S&P 500 Global Clean Energy index was up 275%. From Biden’s inauguration in January 2021 through the end of 2023, the S&P 500 Energy index almost doubled, and the S&P 500 Global Clean Energy index was down -50%3. So had you positioned your portfolios before or even after Trump or Biden was elected to “take advantage” of the advertised policy agendas, you would have performed very poorly.

Often, external macro forces or just simple economic supply/demand dynamics in a capitalist system can overwhelm policy agendas and take over and drive results. For example, during the Trump administration, renewable energy stocks benefited from enthusiasm about growing innovation in the sector, ultra-low interest rates that helped finance those innovations, and the rise of ESG investing 4. At the same time, COVID-19 crushed the price of oil, which fell to about $15.50 per barrel in March 2020 compared to an average of about $57.50 from January 2017 to January 2020.5

For the Biden administration, the price of oil continued its recovery from COVID-19 but then was shocked by the Russian invasion of Ukraine. Oil prices spiked from about $92 per barrel to over $120 per barrel, which was a 33% increase during a two week stretch at the beginning of the war.5 Additionally, due to the rise of ESG investing, some traditional energy companies changed their behavior and stopped growing at all costs, which impacted supply dynamics and added to elevated oil prices. Lastly, inflation started to impact input costs of many industries, which was met by the Fed raising interest rates, which had the negative impact of making the financing of renewable energy projects more expensive.

In summary, based on the above information, we don’t believe it’s possible to time the market around political changes or policies in Washington. It’s more effective to focus on your long-term goals and design a well-diversified portfolio.

GLOBAL MACRO TENSIONS

Geopolitical risks tend to capture headlines (If it bleeds, it leads). While geopolitical risks can have a whole host of impacts on economic activity and markets, geopolitical events are inherently unpredictable, and their impact on financial markets can be highly variable. While certain events may cause market fluctuations or increase volatility over the short term, the long-term effects are often uncertain. Making hasty portfolio decisions in response to geopolitical risks may lead to knee-jerk reactions resulting in missed investment opportunities and/or unnecessary losses.

As seen above, historical data shows that markets tend to recover quickly from geopolitical shocks. Furthermore, a myopic focus on geopolitical risks may cause investors to overlook broader economic trends and fundamentals that have a more profound impact on long-term returns. These include items like GDP growth, inflation rates, and corporate earnings, which all play important roles in shaping market performance. Studies have shown that these factors have a more consistent and lasting influence on investment outcomes compared to short-term geopolitical developments. Additionally, despite historical geopolitical shocks, the market has tended to move up and to the right.

As a result, we believe investors should not use geopolitical risks to drive portfolio adjustments. By maintaining a diversified portfolio that considers a range of outcomes, we believe investors should be better positioned to weather geopolitical uncertainties. We can’t predict when geopolitical risks will happen, but we can be prepared with a diversified portfolio.

WRAPPING IT UP

As we often state, we believe in the power of diversification. Through diversification, our goal is to provide our clients with peace of mind by building portfolios that are resilient to various market conditions. We also believe adopting a long-term investment perspective is essential for wealth creation, as the effects of compounding returns cannot be understated.

Now for our last thought on managing through the noise. We believe the list of events from the 1960s we presented at the beginning of this Insight is especially appropriate. It not only included political and cultural tensions, but also the Vietnam War and the Cuban Missile Crisis—either of which could have ended terribly with the exchange of nuclear weapons. Below we captured those events and the S&P 500’s path in the 1960s. Despite the decade’s considerable “noise,” you’ll notice that the markets continued to rise. History has shown that while uncertainty and noise are inevitable, markets have a remarkable ability to persevere. We remain committed to guiding our clients through these challenges with a steadfast, long-term approach. Should you have questions about partnering with Lee Financial, please reach out to set up a complimentary meeting with us.

A copy of this post is available for download here.

Sources:

1 “Mag 7” or Magnificent Seven Stocks include: Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla

2 Past performance is not indicative of future results.

3 How Much Does Policy Influence Sector Performance? by J.P. Morgan Asset Management, January 2024.

4 ESG investing, or environmental, social and governance investing, is a method of evaluating companies for investment based on their performance on environmental, social, and governance (ESG) metrics. The metrics are meant to assess a company’s sustainability and ethical impacts.

5WTI Crude Oil price per barrel; FactSet

6 The 1962 the stock market decline is often referred to as “the Kennedy Slide”. It was driven by several factors including: (1) economic uncertainty as post-war expansion was beginning to show signs of weakness. (2) government policies from JFK worried Wall Street and were thought to be anti-business. (3) rising interest rates from The Federal Reserve tightening monetary policy. (4) Cold War tensions and (5) speculative excess – In the late 1950’s and early 1960s there was a speculative bubble with some smaller companies seeing sharp increases in valuations not justified by fundamentals. Investor confidence returned toward the end of the year.

7 The 1966 the stock market saw numerous factors impacting investor sentiment. These included: (1) rising inflation, (2) tightening monetary policy, (3) stagnating corporate earnings, (4) geopolitical uncertainty from the Vietnam war and Cold War, (5) market valuation concerns.

8 Morningstar Direct data as of 09/30/2024

_ _

Disclaimer:

Please remember that past performance is not indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by LFC), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from LFC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. LFC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the LFC’s current written disclosure statement discussing our advisory services and fees is available upon request. If you are an LFC client, please remember to contact LFC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services.

The views expressed herein are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.