Higher volatility has been an investment theme of ours since 2025, and it remains one for 2026. The word “volatility” makes a lot of investors nervous. It shouldn’t, and here’s why.

Volatility and risk are two terms that get used interchangeably in financial media all the time. They are not the same thing and confusing them is one of the costliest mistakes an investor can make.

Risk is the possibility of a permanent loss of capital — you bought something for $100, sold it for $80, and that loss is locked in. Warren Buffett defines it exactly this way. Risk can be managed through diversification.

Volatility, by contrast, is simply how quickly and how often the price of an asset moves. It may result in a loss or a gain. And importantly, it cannot be minimized. It is a permanent, unavoidable feature of markets.

The confusion between the two traces back to academia. When Modern Portfolio Theory emerged in the early 1950s, economists needed a measurable proxy for risk, and price change was far easier to quantify than underlying asset value. So, volatility became the stand-in for risk. That shorthand stuck, but it was always an approximation, not a fact.

MARKETS ARE ALWAYS VOLATILE

If you’ve been investing for any length of time, you’ve lived through events that felt catastrophic in the moment: the dotcom collapse, the 2008 financial crisis, COVID-19, the 2023 regional banking crisis, 2025 liberation day. Each one arrived with alarming headlines and sinking feelings. Each one eventually passed.

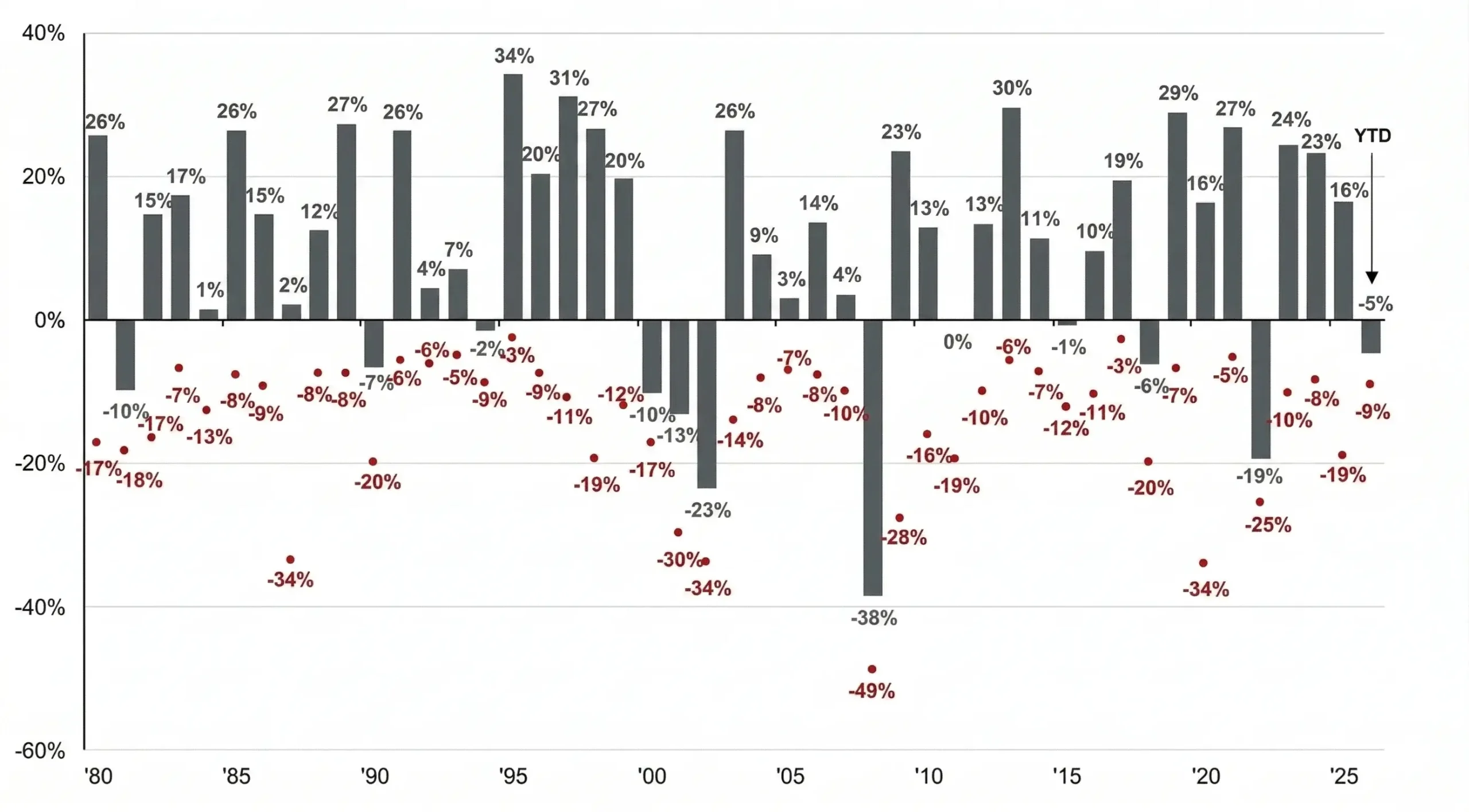

As seen below, history bears this out. Despite an average intra-year drop of 14.2%, the S&P 500 has delivered positive annual returns in 35 of the last 46 years. Every single year experienced some degree of decline, ranging from -3% to -49% and yet, the long-term trajectory remained upward. Volatility was always present. The investors who succeeded were the ones who stayed the course through it.

S&P 500 Intra-Year Declines vs. Calendar Year Returns

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management. Past performance is no guarantee of future results.

Guide to the Markets – US. Data are as of March 31, 2026.

WHY OUR BRAINS WORK AGAINST US

Understanding volatility intellectually is one thing. Managing your reaction to it is another.

Behavioral economics gives us a useful concept here: loss aversion. Research by Daniel Kahneman and Amos Tversky found that losses feel roughly twice as powerful, psychologically, as equivalent gains.1 This isn’t a character flaw, but rather it’s evolutionary wiring. For our early ancestors on the Serengeti, losing a day’s food could be fatal; gaining an extra day’s food was merely nice. Our brains learned to weight losses heavily, and that instinct still governs us today, even when the “loss” is a temporary dip in a brokerage account.

This bias is precisely what drives investors to make their worst decisions: selling into declining markets and buying back in after the recovery is already underway. It’s the classic trap of buying high and selling low, not out of bad intentions, but out of a very human emotional response to price movement.

THE COST OF TRYING TO DODGE VOLATILITY

Many investors believe they can sidestep volatility by moving in and out of the market at the right moment. The data tells a different story.

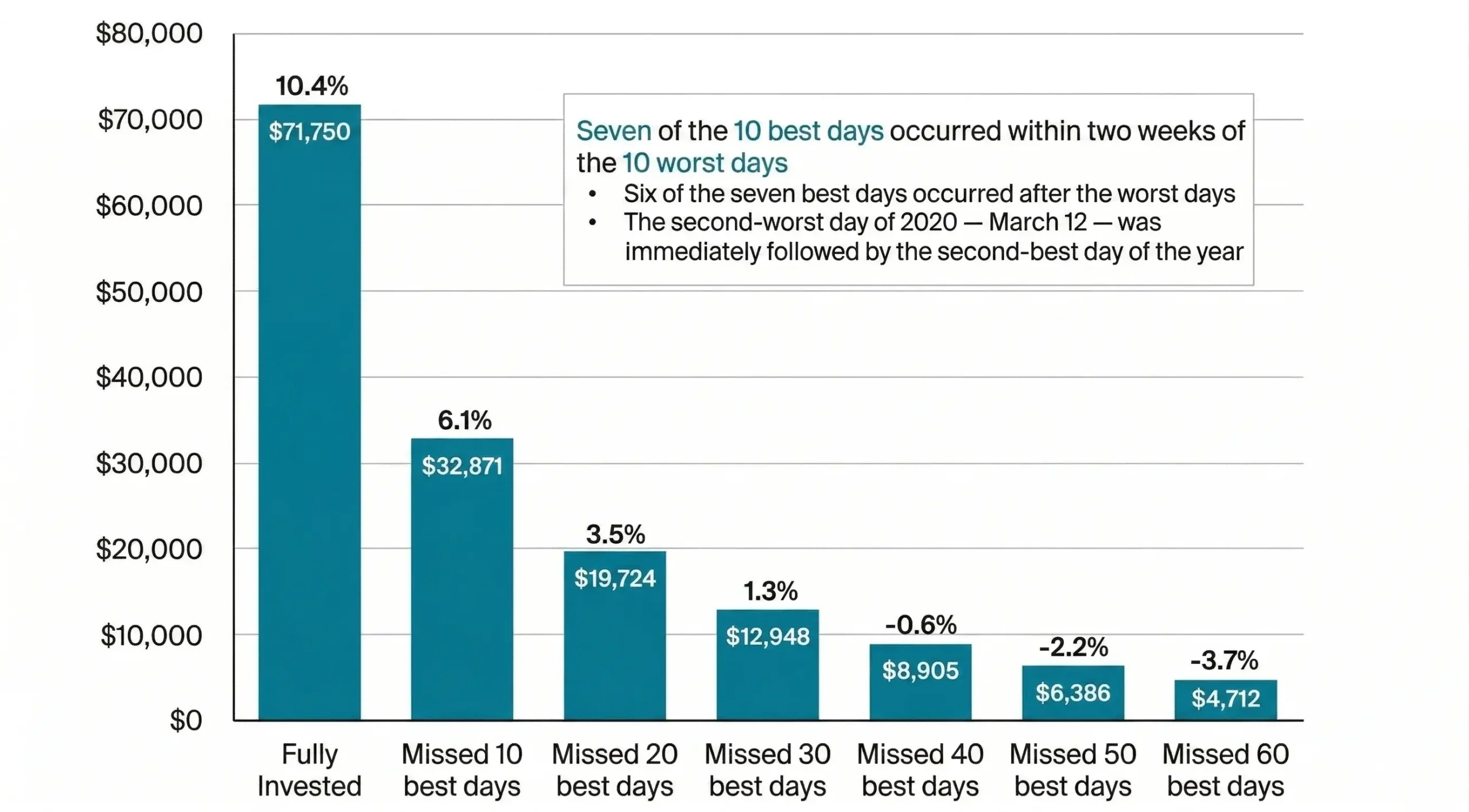

Impact of Being Out of the Market

Returns of the S&P 500

Performance of a $10,000 investment between January 3, 2005 and December 31, 2024

Source: J.P. Morgan Asset Management using data from Bloomberg. Past performance is no guarantee of future results.

Guide to the Markets – US. Data are as of December 31, 2024. 2

Consider this: over a 20-year period, a fully invested position in the S&P 500 grew a hypothetical $10,000 investment to $71,750, a 10.4% annualized return. Miss just the 10 best days over that same 20 years, and that return falls to 6.1% leaving you with $32,871 instead. Miss the 20 best days and you’re at 3.5%.

Here’s the crucial detail: 7 of the 10 best days in the market occurred within two weeks of the 10 worst days. That means the investors who sold during the worst moments were almost certainly not back in the market in time to capture the best ones. Trying to avoid volatility doesn’t protect you from it, it just ensures you absorb the downside while missing the recovery.

WHAT TO DO INSTEAD

The antidote to loss aversion isn’t to suppress your emotions, it’s to understand them, prepare for them, and have a plan that doesn’t depend on them.

- Ride it out. Knowing that loss aversion is a hardwired bias itself is a form of protection. When the urge to sell feels overwhelming, recognize it for what it is.

- Step back from financial media. Headlines are designed to generate clicks, not calm. Sensationalism amplifies loss aversion. Reducing your exposure to market commentary during volatile periods can meaningfully reduce anxiety.

- Check your statements less frequently. The more often you look at short-term price movements, the more opportunities loss aversion has to influence your decisions.

- Match your investments to your time horizon. If you have a near-term financial need, it should be in lower volatility assets. Long-term goals can absorb volatility in exchange for higher expected returns.

Volatility is not your enemy. It is the price of admission to long-term returns. The investors who learn to sit with discomfort, tune out the noise, and stay invested are the ones who tend to reach their financial goals.

“Volatility is actually the opposite of risk. It’s opportunity. But you need to think

through and fight some basic human weaknesses.”

— Jeff Ubben, ValueAct Capital

That fight is worth having.

As always, please contact a member of your Lee Financial team if you have any questions.

Marco Rodriguez, CFA

Co-Chief Investment Officer

1 Prospect Theory: An Analysis of Decision under Risk by Daniel Kahneman and Amos Tversky

2 Returns are based on the S&P 500 Total Return Index, an unmanaged, capitalization-weighted index. The hypothetical performance calculations are shown for illustrative purposes only and are not meant to be representative of actual results while investing over the time periods shown. Past performance is not indicative of future returns. An investor cannot invest directly in an index.

DISCLAIMER

Please remember that past performance is not indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by LFC), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from LFC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. LFC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the LFC’s current written disclosure statement discussing our advisory services and fees is available upon request. If you are an LFC client, please remember to contact LFC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services.

The views expressed herein are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities